2023 HOUSE PRICES AUSTRALIA: RISING DUE TO HOMEBUYERS SCHEMES?

Make 2023 The Year You Start Your Journey As A First Home Buyer

Will house prices rise or fall in 2023 across Australia?

Over the years, I’ve seen numerous things which have driven up the demand for housing, home ownership, and house prices.

In this video, I’m going to talk about the 2023 house prices Australia and the effects of new government schemes on the property market, why they exist, and how these schemes increase the leverage and therefore, the property prices.

I’m also going to go over the crazy new ones, and when are these going to affect the property market or the 2023 house prices Australia in particular.

Let’s get into it!

First Home Buyers Scheme: why do they exist?

So firstly, they exist because our economy favours those who already own property.

What this has meant in the past is that property values have gone up much faster than what incomes have.

As a result, it’s harder for people without property to buy a property because they have to continuously save larger deposits to get into the property market.

If property keeps going up faster than wages, then eventually no one is going to be able to afford a property. This has been the common thinking for a long time now. But lo and behold, the government keep on bringing out ways to get first homebuyers into the market while house prices keep on increasing.

Let’s go back to the mother of modern government grants and schemes – that is the First Home Owner Grant, which was introduced in the year 2000.

These schemes are always introduced as being temporary, but evidently they have a knack of sticking around as it’s still around today.

So from here I can say that first home owners win as they can get in the market. Existing property owners win as it creates more demand for property and pushes the price of houses higher, and the government wins because it gets the votes it craves.

So, let’s go and take a step back and just tease out how existing property owners win. This is the core point of this video.

How Existing Property Owners Win

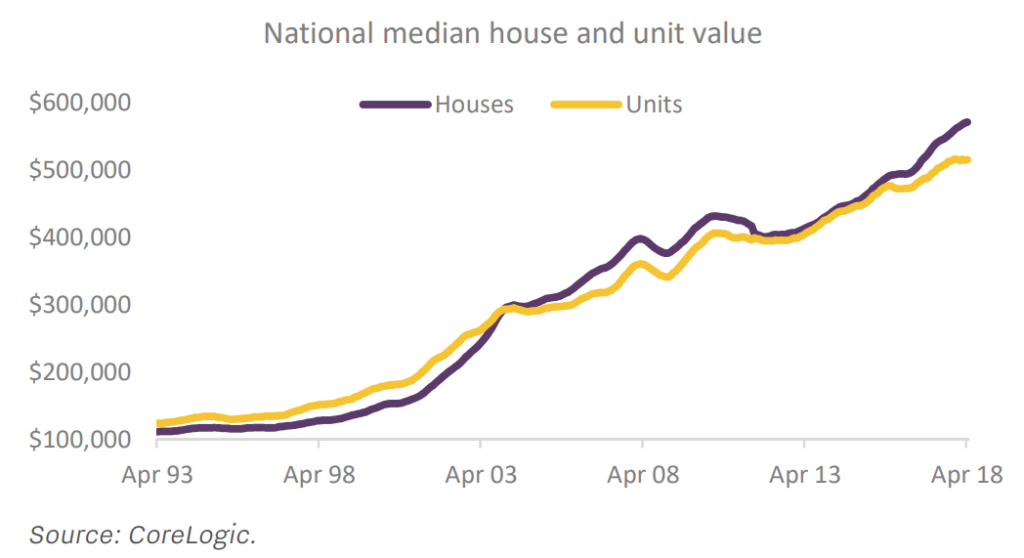

Firstly, you can just look at this graph of the Australian residential property prices since 2000.

I know there are several factors contributing to property prices but since 2000 one of the majors have been the first home owner grants and schemes.

I want to explain the leverage thing because it’s important.

If you buy a house, you can typically borrow 90% of the value of the property that you’re purchasing. In some cases you can go higher but let’s just use 90% for this video. This means all you need to do is put in 10% plus whatever costs you need to settle.

So, if the government gives you $10,000, you could effectively buy something for $100,000, borrow 90% which is $90,000 and then you would put in the rest which is your $10,000 government grant.

This is one of the things that are pushing the housing market forward. If you didn’t have these grants, people would not be able to offer the prices that they do. So these grants give the buyers access to this game so they can bid up the property prices.

The Crazy New Government Schemes

Next, let us talk about the crazy new schemes from the government.

First, we have these schemes from NHFIC. Before I go to the schemes, NHFIC or National Housing Finance and Investment Corporation is the government organization dedicated to aid housing concerns and is responsible for the distribution of these grants to get home buyers into the market all across the country.

NHFIC have these main schemes – the New Home Guarantee, First Home Guarantee, and the Family Home Guarantee.

That’s right. It’s now become so complicated that there’s even actually a separate organization to administer all of these handouts.

They’ve even stated this year that they would move the amount of spots on these schemes from 35,000 to a max of 50,000. That’s a 40% increase in the amount of spots available in one year!

That is a massive increase, and what it does is that it increases the demand by a massive amount, too.

The problem is we’ve already seen from 2020 to 2021 what that increased demand did because in those years we had a shortage of property on the market.

When the market shortages kick in, this is just going to push 2023 house prices Australia further and further.

The other one is the crazy communist Co-Buy Schemes. Let me explain what they are.

So, Anthony Albanese, our current Prime Minister, put through an election promise to set up a 40% co-buy scheme.

What does that mean? It means the government will help you buy your house and pay for up to 40% of that house with you.

That’s the reason why I’m saying “crazy communists co-buy schemes”. If they push it just a little bit further – and that’s what they do – they push these schemes further. They’ll be buying the majority of your own home and that’s not good if the government owns a majority of your own home.

Now there are other state government schemes that are added to the paradigm.

Dominic Perrottet has announced the First Home Buyer Choice as a part of an integrated multi-billion dollar housing package in New South Wales.

Daniel Andrews’ government has announced an investment in public and affordable housing scheme in Victoria.

Firstly, some people will come back and tell you these schemes are all limited and they’re only temporary. Well, go back to the year 2000 and you’ll hear the same arguments said about the First Home Owner Grant.

It was then argued that it would help offset costs of Capital Gains Tax changes.

Anyway, the point is IT’S STILL here. It’s now 22 years old. That’s a bit longer than temporary.

So mark my words, these new Co-Buy schemes will come in as limited at the start, but what will happen is they’ll get extended just like the First Home Owner Grant.

So, let me spell this out. Under a 40% Co-Buy scheme, if you can afford a $600,000 loan, the government will pitch in 40% or $400,000 then you could buy a $1 Million property.

If you’re going to pretend that this isn’t going to affect the housing market, then you’ve got to be kidding me.

I hope I’ve really made that clear and if you like this content and you’re getting something out of it, please comment, like, and subscribe. That helps us a lot.

So, will house prices go up in 2023?

I guess the next question is when will be the next property market boom? I’m pretty sure that’s the question in the mind of almost every Australian that’s way crazy about property.

What I want to say is first hold your horses. We have some pretty strong headwinds in our economy and the property market, and the main one there is the rising interest rates.

The Reserve Bank is still telling us they’re going to continue to raise these interest rates to put out the higher levels of inflation. Who knows what the future’s going to hold?

This is why it makes things very hard to predict.

I just think that when the next boom comes, these schemes and grants are going to be a major contributing force to the property market going to an unthinkable high.

Wrap-Up

Now, I will say a few things here before I close this out.

Number one, none of this is financial advice to the property market.

Number two, property market boom does not mean a strong economy – and this is one thing that people will tell themselves because they want to get greedy.

Number three, if you like this, and if you’re watching now, you need to click the like and subscribe button and support the channel.

That’s all for me for today. Till next time. Cheers!

Will Bell

Will Bell has 15 years’ experience in the finance industry, the last 11 years he has owned and operated Will Bell Mortgage Broker. He specializes in residential home loans and over the years has carved out a trusted brand. This is proven by the reviews his customers have made regarding the service and the experience he has provided.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.