AUSTRALIAN PROPERTY BUBBLE 2023: Are we expecting a burst soon?

Make 2023 The Year You Start Your Journey As A First Home Buyer

Australian Property Bubble

Over the last 20 or 30 years the Australian property market has been elevated to religious status.

The prosperity promised by investing in real estate in Australia has had many effects such as the rise of the horde of property spruikers and an Australian property bubble that has apparently been about to pop for more than 15 years.

As a country we have structured our system to reward people who invest in real estate and over that time Australia has prospered and investors have been richly rewarded.

Fast forward to present day, we are going through the steepest and fastest interest rates rise of all time and it leaves us begging the question,

“Is the party over? Did we get caught asleep at the wheel? Is the housing market going to crash?”

In this video we’re going to take a look at the current state of play and ask,

“Are we seeing the bursting of an Australian property bubble in 2022 and 2023?”

Over the past 15 years the warning lights have been flashing on our overall indebtedness. The ratio of property values to household income has been constantly climbing as the doomsayers love showing us a proof of the 2022 Australian property bubble that’s about to pop.

All of this has been brought about by 25 odd years of reducing interest rates and the fact that Australia’s average income is actually very high compared to the rest of the world. You can thank the world’s demand for resources for that.

But, can it continue? We now have a different global situation than what we had before.

The demand from China has stalled and the relationship made worse when our leaders called for a transparent review as to what went on in Wu Han.

China is important because in 2020 they took a massive 40.7% of all of our exports.

The argument that this is just a large bump in the road is that China still need to finish their belt and road initiative which has still got another 30 odd years till completion, meaning they still need heaps of our resources.

Can China buy enough from us to cushion this property slump?

The answer to that would be no, given China’s economy is on rocky territory as well. However, I wouldn’t rule out Chinese demand to play a major factor in future booms in the property market.

Actually, China is a good segue into the rising cost of living which can also be translated to rising interest rates.

Because supply lines have stalled, it has naturally pushed the prices of things up. Even when things have cost the same to buy overseas, the cost to import them back has increased due to increased gas and oil prices to transport them combined with added insurance costs due to the global instability.

The fact is the cost of stuff has gone up. This is not just a problem here but all over the world and the answer of central banks all around the world is to increase interest rates. The idea behind that is to reduce demand for goods and services in order to bring down the cost of things.

A bold move given that these solutions will not solve the supply issues I just mentioned. Anyway, that’s what’s happening, and the rising interest rates are the central factor in this property price bubble.

The value of the property market is directly related to the supply and demand of money.

Rising interest rates means the supply of money will reduce and therefore property values will go down but the question is by how much?

Before I speculate about real estate price drops I’m going to address some of the supporting factors for the property market.

Factors that Affect the Australian Property Market

1. High Immigration

Immigration clearly plays a role in the demand for property. However, I think the effects of immigration are not going to kick in for a while until our doors are fully open. Once that happens we will see rents increase and if interest rates ease then the property market will grow again.

But that is the next cycle. Immigration will not affect property short term. If you want to understand more about the effects of immigration and other factors on the next property boom I have made other videos that are worth watching.

2. Low Supply

At the moment, there is still a fairly low supply of properties in Melbourne and the rest of Victoria.

I think that what we are seeing is, property owners are holding on to their properties because they believe the property market will boom again in the future.

What we don’t know is how high will home loan interest rates go.

There is a point at which people cannot maintain their debt repayments and are forced to sell. If this creates an oversupply then property prices will eventually drop more.

This is what underpins the fears of the cult of the 40% drop and the property market bubble popping.

Which brings us to the next cushioning factor which I think is the most important. This is kind of anti-intuitive because it’s the same thing that’s making things hard for us right now.

And that is the Reserve Bank of Australia and the Federal Government.

3. The Reserve Bank of Australia and the Federal Government

Once the property market drops by a certain amount, you will have either or both the RBA and the Federal Government take action to support the property market and the broader economy.

There is the argument to say that the RBA will have trouble getting inflation down as it has all been caused by outside factors like China, the war, energy prices and the pandemic.

I get that. There will be a point however where the central bank must change policy because in their eyes the results of keeping interest rates high will be worse than dropping them again.

It’s useful to look at history and understand that the role of government is to support the economy when times get nasty.

The UK central bank a couple of weeks ago is the latest example of that.

This is a classic boom-bust cycle so what would be pertinent to do is look at previous property market declines.

The question is how much will the property market go down before it goes up again?

How much will the Australian property bubble tank in 2022 or 2023?

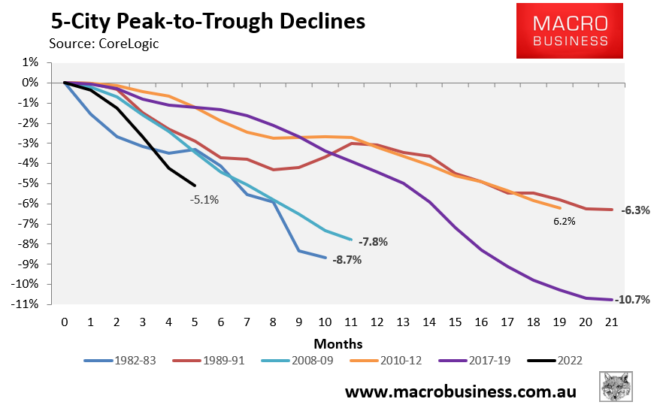

This data is the main point that I will go back to here because it tells us a quite lot about the past. And Mark Twain once said something like history doesn’t repeat itself but it does rhyme.

Take a look at the peak-to-trough prices on this graph. It’s pretty crazy, huh?

The first thing that stood out to me was how small these dips are. I went back to the GFC because that was around the time I bought my first home. It’s very surprising that the dip that spread across the 5 major cities was 8.7% in 2008 and 6.2% in 2012.

I must admit I was skeptical when I first saw this because it didn’t feel right.

It felt like the value of my house ping-ponged around, skyrocketing up 25% before dipping then going back up again before eventually dipping into the start of the cycle around 2012 or 2013.

So I did some basic googling and when you check the graph that period was a great time for property.

It’s interesting that the data smoothes out the volatility that you get in individual markets.

Sometimes, it pays to zoom out so you can see the forest for the trees.

Anyhow, that graph also shows us that this is our steepest decline so far.

The worrying thing here is that we’re currently going through the fastest interest rate increases in Australian history.

In my mind there’s no doubt that the affect of the interest rate rises have not yet been seen on the property market.

What can I say about the Australian property market?

When you understand money creation, you understand that it all gets created as debt. Most of the debt we have created apart from stimulus is through lending to home loans.

Common sense would tell me that if we keep raising interest rates then less money enters the economy because people cannot borrow as much as interest rates increase.

This reduced flow of liquidity to the markets will eventually show up in the stock market and then we will reach peak panic. At this stage, I would expect the central bank to step in and change it’s policy around interest rates.

Also at this time we are likely to see the government come out with more stimulus.

We’re are living through one of those times in history that is going to be remembered well into the future.

When I zoom out I realise that as a nation we are becoming very welfare dependent. To give you an example, we now see cash handouts and mortgage repayment pauses every time there is an emergency, which is actually fairly often.

It’s happening right now with the Victorian floods. The Victorian government doesn’t have this money. It’s basically created as a debt and the next generations will have to worry about paying it back.

This is what our federal government will do if things escalate too much. They will backstop the market before things get too bad.

What does too bad look like? I don’t know but I get the feeling we’re about to find out.

If you want to find out more about the property market crash you might want to watch this video where I discuss the predictions that the property market will drop by 40%. (Click here to watch)

Also, don’t forget to like and subscribe so I can keep creating this content.

Will Bell

Will Bell has 15 years’ experience in the finance industry, the last 11 years he has owned and operated Will Bell Mortgage Broker. He specializes in residential home loans and over the years has carved out a trusted brand. This is proven by the reviews his customers have made regarding the service and the experience he has provided.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.